Your offer just got accepted, and the celebration lasted about ten minutes before the panic set in: now what? Nobody hands you a schedule, yet the next 30 to 45 days are packed with deadlines that can cost you real money if you miss them. This guide walks you through what happens after offer is accepted on a house — week by week, in plain language — so you always know what’s coming, what it costs, and what can go wrong.

After your offer is accepted on a house, you sign the purchase agreement, deposit earnest money into escrow (usually within 3 days), then schedule a home inspection within the first 7–10 days. Your lender orders an appraisal and moves your file into underwriting. Once you receive “clear to close,” you do a final walkthrough, sign closing documents, pay your down payment and closing costs, and get the keys — typically 30–45 days after acceptance.

Key takeaways

- Your earnest money deposit is usually due within 1–3 business days of acceptance — have the funds ready before you make offers.

- Schedule the home inspection immediately; most inspection contingencies expire 7–10 days after the contract is signed.

- Your lender needs a full mortgage application within days of acceptance — the appraisal and underwriting can’t start without it.

- Do not open new credit, change jobs, or move large sums between accounts until after closing; underwriters re-check everything.

- “Clear to close” is the real finish line — until you have it in writing, your closing date is a target, not a promise.

- The final walkthrough happens 24–48 hours before closing and is your last chance to confirm the home’s condition matches the contract.

The first 72 hours: signatures, earnest money, and escrow

The first three days after acceptance are about making the deal legally real and financially serious. When the seller signs your offer, it stops being an offer and becomes a purchase agreement — a binding contract with dates in it. Read it again that same evening. Every deadline in your next six weeks lives in that document: the inspection contingency period, the financing contingency date, the appraisal deadline, and the closing date itself.

Your first hard deadline is the earnest money deposit. In most US markets, you’ll wire 1–3% of the purchase price to an escrow or title company within one to three business days. On a $350,000 home, that’s $3,500 to $10,500 leaving your account almost immediately. Escrow simply means a neutral third party holds the money — neither you nor the seller can touch it until the contract says who gets it. If the deal closes, it counts toward your down payment. If the deal dies for a reason your contingencies cover, you typically get it back. The contract language decides every one of those scenarios — which is why it’s worth reading our guide on how to understand real estate purchase agreements in Canada and the US before you sign.

Two more things happen in this window. Your agent “opens escrow” or orders title work, which starts a title search — a records check confirming the seller actually owns the home free of undisclosed liens. A responsive agent matters enormously in these first days; if yours has gone quiet, here’s how to find a realtor you can trust. And you should notify your lender the moment the offer is accepted, because the mortgage clock is the slowest-moving part of the entire timeline.

Week one: the home inspection can reshape the whole deal

Week one belongs to the inspection, and it’s the single most consequential appointment you’ll book. Most contracts give you 7–10 days from acceptance to complete inspections and either accept the home, negotiate repairs, or walk away. That window is short, and good inspectors book up — so call the day your offer is accepted, not the following week.

A general home inspection runs roughly $350–$600 depending on your market and the home’s size, and takes two to four hours. You should attend. Walking the property with the inspector teaches you more about your future house than any document will — where the water shutoff is, how old the furnace actually is, which “small” stain is hiding a roof problem. Depending on what the general inspection flags, you may add specialty inspections: sewer scope (about $150–$300), radon test, termite inspection, or a structural engineer’s review.

When the report lands, resist the urge to panic. Every inspection report looks alarming because inspectors document everything, including $12 fixes. What matters is separating cosmetic noise from the five categories that deserve negotiation: roof, foundation, electrical, plumbing, and HVAC. And cross-check the findings against what the seller told you upfront — our guide on how to interpret property disclosure statements shows exactly what sellers are required to reveal, and what a mismatch means.

From here you have three moves: proceed as-is, request repairs or a credit, or exercise your inspection contingency and exit with your earnest money. A repair credit is often smarter than asking the seller to do the work — a seller patching a roof to satisfy a contract has very different incentives than you hiring your own roofer after closing.

Weeks one to two: mortgage application, locked rates, and the appraisal

While the inspection drama plays out, your financing needs to move in parallel — and this is where buyers lose the most time. A pre-approval is not a mortgage. It was an estimate based on a preliminary look at your finances; now the lender needs a complete application tied to this specific property. Under US federal rules, once you submit a full application, your lender must send you a Loan Estimate within three business days — a standardized form showing your projected rate, monthly payment, and closing costs. The Consumer Financial Protection Bureau explains exactly what to check on it in its Loan Estimate guide.

This is also when you decide whether to lock your interest rate. A rate lock freezes your quoted rate for a set period — typically 30, 45, or 60 days. Match the lock to your closing date with a small buffer. A 30-day lock on a 45-day closing is a common and expensive mistake, because lock extensions typically cost 0.125%–0.375% of the loan amount.

Around the same time, the lender orders an appraisal: an independent professional’s opinion of the home’s market value, which you pay for (usually $500–$800) but the lender controls. The appraisal protects the lender, not you — they won’t loan $400,000 against a house their appraiser says is worth $370,000. If the appraisal comes in below your contract price, you have four options: the seller drops the price, you pay the difference in cash, you split it, or your appraisal contingency lets you exit. In hot markets, appraisal gaps kill more deals than inspections do.

Weeks two to four: underwriting, the quiet stretch that decides everything

Underwriting is the part of the process nobody warns you about, mostly because nothing visible happens. An underwriter is the person at the lender who verifies every claim in your application — income, assets, debts, employment, the appraisal, the title work — and decides whether the loan actually gets funded. Files typically sit in underwriting for one to three weeks, and the silence is normal.

What isn’t normal is ignoring document requests. Underwriters issue “conditions” — requests for a bank statement, a letter explaining a deposit, an updated pay stub. Every day you sit on a condition is a day added to your closing. Answer the same day, even when the request seems absurd. Yes, they really do want a signed letter explaining the $900 your aunt e-transferred you in March.

This is also the stretch where buyers accidentally destroy their own deals. Underwriters pull a fresh credit report shortly before closing, and they compare your current finances to your application. New financing of any kind — a car loan, a furniture store card, even a “12 months no interest” appliance plan for the new house — changes your debt-to-income ratio and can void your approval days before closing.

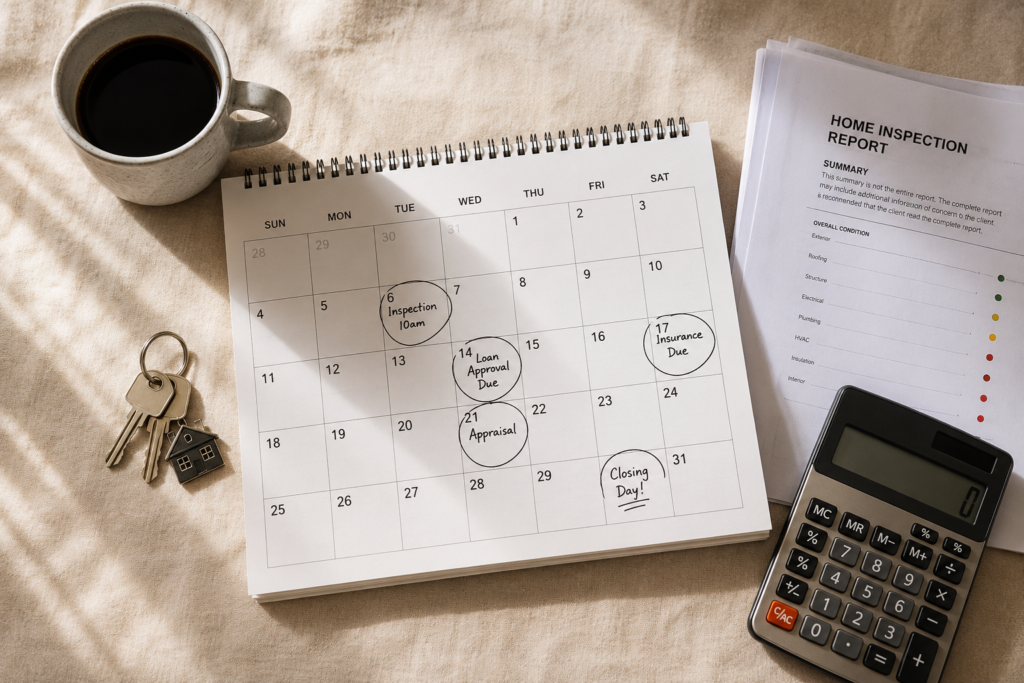

The final week: clear to close, the walkthrough, and closing day

The last week compresses three milestones into a few days, and each one has a specific job. The first is clear to close — the underwriter’s formal sign-off that every condition is satisfied and the loan is approved for funding. Until those words arrive in writing, your closing date is aspirational. Once they do, the closing agent schedules signing.

At least three business days before closing, US lenders must deliver your Closing Disclosure — the final version of your numbers. Compare it line by line against your Loan Estimate. Fees shouldn’t have drifted much, and some legally can’t increase at all. If something looks wrong, this three-day window exists precisely so you can question it. And remember the spending doesn’t stop at the closing table — our breakdown of the hidden costs of homeownership covers what’s waiting after the keys.

Then comes the final walkthrough, usually 24–48 hours before closing. This is not an inspection redo. You’re verifying three things: the home is in the same condition as when you contracted, agreed repairs were completed, and everything the contract says stays (appliances, fixtures, that shed) is still there. Run the taps, flip the breakers, test the HVAC, open the garage door. If something’s wrong, you deal with it before signing, not after — a repair credit or an escrow holdback negotiated at the table beats chasing the seller once the deed is recorded.

Closing day itself is administrative. You’ll wire your down payment and closing costs (verify instructions by phone — again), sign a stack of documents 40–100 pages deep, and wait for “funding and recording”: the lender releases the money and the county records the deed in your name. In dry-funding states, that can take until the next business day. Then, and only then, the keys are yours.

The full timeline at a glance — and what can delay it

Here’s the entire post-acceptance process condensed into one table, with the typical windows for a financed purchase in the US. Cash purchases compress dramatically — often 7 to 14 days — because everything lender-related disappears.

Delays are common and usually survivable. The usual suspects: appraisals coming in late or low, underwriting conditions that buyers answer slowly, title defects like an old lien that was never released, seller-side problems (their next purchase falls through), and insurance surprises in wildfire or flood zones where binding a policy takes longer than expected. Most delays cost days, not deals — but a seller isn’t obligated to grant extensions, which is why answering your lender fast is genuine self-defense. And if you’re worried about the seller getting cold feet: once both sides have signed, walking away without legal grounds is rare — and expensive for them when they try.

Common mistakes buyers make after the offer is accepted

1. Treating the pre-approval as finished financing

Buyers relax after acceptance because “the mortgage part is done.” It isn’t — it hasn’t started. The full application, appraisal, and underwriting all happen after acceptance, and slow document turnaround is the number-one buyer-caused delay. Submit your complete document package within 48 hours of acceptance and treat every underwriter request like it’s due the same day, because functionally it is.

2. Scheduling the inspection “when it’s convenient”

Waiting five days to book an inspection inside a ten-day contingency leaves no room for a specialty follow-up. If the general inspector recommends a sewer scope or a structural engineer on day eight, you’re now begging the seller for an extension — from a position of zero leverage. Book the general inspection within 24 hours of acceptance and hold day 7–8 open for follow-ups.

3. Letting the rate lock expire before closing

Intermediate buyers know to lock a rate; they forget locks expire. A 30-day lock on a closing that slips to day 38 means paying an extension fee or re-locking at current rates — which, if rates moved against you, can add real money to every payment for 30 years. Lock for your full contract timeline plus a 5–10 day buffer, and calendar the expiry date yourself.

4. Making big, well-intentioned financial moves

The classic version isn’t reckless spending — it’s the buyer who finances new appliances “for the house” or accepts a better job offer three weeks before closing. Both can void an approval, because underwriters re-verify employment and credit right before funding. If a genuinely unavoidable change is coming, tell your loan officer immediately; surprising an underwriter is always worse than warning one.

5. Skipping or rushing the final walkthrough

Buyers waive the walkthrough because “we just saw it at inspection” — five weeks, one moved-out seller, and one hastily patched wall ago. Fifteen minutes of testing taps, HVAC, and garage doors is the cheapest insurance in the entire transaction. Once you sign, problems that were the seller’s obligation become your weekend project.

FAQ: what happens after offer is accepted on a house

How long after an offer is accepted do you close?

For a financed purchase in the US, plan on 30–45 days from acceptance to closing. Cash purchases can close in 7–14 days because there’s no lender, appraisal, or underwriting. Your actual date is written in the purchase agreement, and both sides must agree in writing to change it.

Can I back out after my offer is accepted?

Yes, if a contingency in your contract covers your reason — inspection findings, a low appraisal, or financing falling through are the common ones. Back out within a valid contingency window and you typically get your earnest money returned. Back out for a reason your contract doesn’t cover, and the seller usually keeps your deposit.

Who pays for the inspection and appraisal?

The buyer pays for both in nearly all US transactions. Expect roughly $350–$600 for a general home inspection and $500–$800 for the appraisal, paid when each service is performed — not at closing. Specialty inspections like sewer scopes or radon tests are extra and also on you.

What does “clear to close” mean?

Clear to close means the underwriter has verified everything — income, assets, appraisal, title — and formally approved your loan for funding. It’s the green light that lets the closing agent schedule signing. Until you have it, your closing date is a target; after it, delays become rare.

Can the seller accept another offer after accepting mine?

Not in place of yours. Once both parties sign, you have a binding contract, and the seller can’t simply switch buyers. They can accept backup offers, which only activate if your deal falls through. A seller trying to walk away without legal grounds risks being sued for specific performance or damages.

What if the appraisal comes in lower than my offer?

You have four options: negotiate the price down to the appraised value, pay the gap in cash, split the difference with the seller, or use an appraisal contingency to exit with your earnest money. Lenders base the loan on the lower of price or appraised value, so the gap must be resolved before closing.

Your next step after the offer is accepted

If you remember one thing about what happens after offer is accepted on a house, make it this: the timeline is driven by deadlines you can control — earnest money, inspection booking, and same-day answers to your lender. Buyers who move fast in the first ten days close on time; buyers who coast lose their leverage exactly when they need it. Pull out your purchase agreement tonight, write every deadline into your calendar, and make sure you’re not walking into any of the top 10 mistakes first-time homebuyers make — then browse the rest of our first-time homebuyer guides as each milestone approaches.

Free guide

Confused by real estate? Get the plain-English guide.

Buying, selling, investing & the legal basics — explained simply in 20 pages. Free, straight to your inbox.

No spam. Unsubscribe anytime.